In a recent post, we discussed how more young adults are waiting longer than previous generations did to get married and how that correlates with decreased homeownership rates among young Americans. Now, recent data from a National Association of Realtors (NAR) survey offers more evidence that first-time homebuyers are less of a force than they once were in the housing market.

On November 3, NAR released their annual survey results, which found that first-time homebuyers accounted for just 33% of the market. That’s the lowest market share since 1987, when first-timers represented just 30% of homebuyers.

First-time buyers are important to the overall strength of the housing market and the economy at large. However, they also face considerable obstacles to buying that first home, including a still-shaky job market and possibly heavy student debt. These factors can make it hard for new buyers to set up a down payment and qualify for a mortgage.

Those young adults are also usually looking for homes near larger cities with a bustling nightlife and better job opportunities. However, home prices are continuing to climb, and strict lending rules are making it tougher for so-called millennials to save up enough for a down payment. According to the NAR survey, 23% of first-time buyers said it was difficult to save for a down payment, and 57% of those respondents said that student loans had delayed their savings. In 2013, 53% of those surveyed cited student loans as a source of difficulty saving for a down payment.

If that wasn’t enough to dissuade potential first-time buyers, NAR Chief Economist Lawrence Yun stated, “Adding more bumps in the road, is that those finally in a position to buy have had to overcome low inventory levels in their price range, competition from investors, tight credit conditions and high mortgage insurance premiums.”

With that many challenges, it’s no wonder young professionals are instead renting, searching for a better income, and waiting to find that special someone before taking the plunge into homeownership.

If the economy continues to improve and wages increase, that may make buying a home more appealing for the millennials. After all, it’s not that the majority of them don’t want a home. According to the U.S. Housing Confidence Survey as reported by Zillow, 65% of respondents aged 18 to 34 said that they consider owning a home a necessary part of living “The Good Life” and the “American Dream,” more than any other age group. More than 80% of renters in this age group stated that they were “confident” or “somewhat confident” that they will eventually be able to afford a home, and more than half expect to buy a home within the next 5 years.

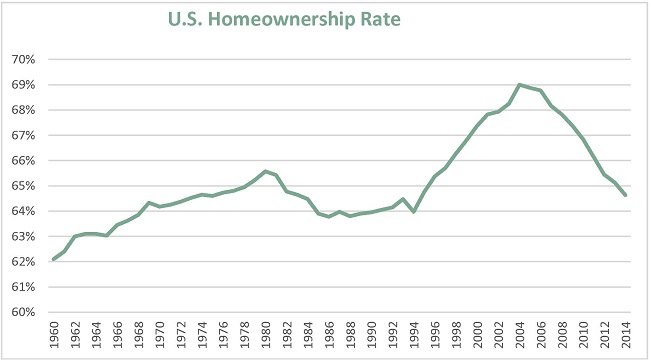

Another factor to consider is whether there might be a natural equilibrium point for homeownership. Considering the chart below of historical homeownership rates in the United States, if we were to look for a sustainable homeownership rate, we might postulate that it would be somewhere around 64%. And since the U.S. Census Bureau’s Housing Vacancies and Homeownership (CPS/HVS) for third quarter 2014 showed a national homeownership rate of 64.4%, perhaps we are approaching a point of stability, though we suspect the homeownership rate is going to drop a bit further before it stabilizes.

Based on data from U.S. Census Bureau Housing Vacancies and Homeownership (CPS/HVS).

What do you think? Do you see the percentage of first-time buyers rebounding in 2015? Do you think the homeownership rate will stabilize, and if so, at what point?

{kind=link}

Recent Comments