Christmas at Rockefeller Center courtesy of petercruise, CC BY 2.0.

After a rough start to the year from an economic standpoint, 2014 looks like it will end well. Many economic indicators are positive, and forecasters seem cautiously optimistic. A recent Bloomberg article announced that the “biggest hiring increase in more than a decade and the lowest gasoline prices in four years are convincing households that the acceleration in economic growth will be sustained.”

According to the latest information from the U.S. Bureau of Economic Analysis (BEA), the U.S. economy grew more than expected last quarter. BEA’s second estimate of annual growth in gross domestic product (GDP) for third quarter 2014 increased by 0.4 percentage point, from 3.5% growth in the advanced estimate to 3.9% in the November 25 update. This change was mainly due to larger than expected increases in both consumer spending and business equipment investment. The advanced estimate for third quarter 2014 corporate profits also shows that profits were up $43.8 billion, although the gains weren’t nearly as large as in the second quarter ($164.1 billion). The third estimate of GDP growth for third quarter 2014 will be released on December 23. If this rise in GDP for July, August, and September is confirmed, following the 4.6% GDP growth in the second quarter, they will be the strongest back-to-back quarters in more than a decade, since the second half of 2003.

Looking ahead, the December Livingston Survey summarizes the forecasts of 29 economists from industry, government, banking, and academia. The surveyed economists have projected that the annualized growth in real GDP for the second half of this year will be 3.1%. That’s up 0.1 percentage point from their prediction in June. The economists also see the unemployment rate falling more than previously predicted; current forecasts are 5.7% unemployment in December 2014 and 5.6% unemployment in June 2015.

Consumer confidence is also approaching pre-recession levels. Since late 1985, Langer Research Associates has produced the Bloomberg Consumer Comfort Index (CCI), currently measured on a scale of 0-100, based on weekly surveys of consumer attitudes. In the week ending December 7, the CCI increased to 41.3, its highest since early November 2007 and not far from its 29-year average of 41.6. Subindexes measuring consumer sentiment regarding the national economy and the buying climate also rose to the strongest levels in 7 years. The preliminary December results of another index, the Thomson Reuters/University of Michigan Index of Consumer Sentiment (ICS), increased to 93.8, the highest since January 2007.

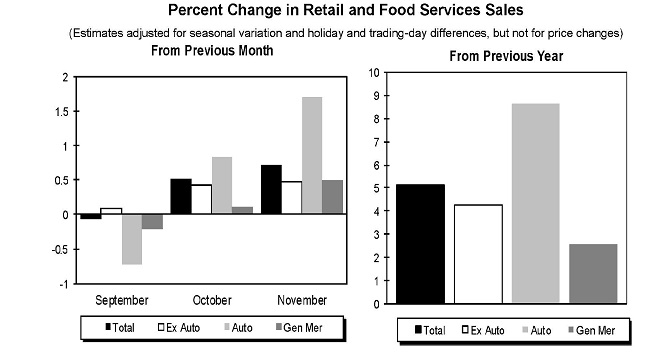

On December 11, the U.S. Census Bureau announced that advance sales estimates of U.S. retail and food services for November 2014, adjusted for seasonal variation and holiday and trading-day differences but not for price changes, were $449.3 billion, up 5.1% from November 2013. Retail sales were up 4.9%, motor vehicle sales were up 9.5%, and nonstore retailer sales were up 8.7% from last November, while gas station sales were down 2.1% over the same period.

Courtesy of U.S. Census Bureau.

Many economists have attributed these positive indicators to the steady employment growth we have seen recently, as well as the oil boom and resulting fall in fuel prices. But regardless of the cause, we hope this good news helps brighten your holidays.

{kind=link}

Recent Comments