SEC Chairman Mary Jo White

It’s been a little over 3 years since President Obama signed the Jumpstart Our Business Startups (JOBS) Act of 2012 into law, enabling more businesses to utilize crowdfunding to raise capital and gauge market interest. As we’ve noted before, while there has been dramatic growth in the number of crowdfunding platforms and the types of opportunities available, many investors have been frustrated at the delays implementing some JOBS Act requirements. However, thanks to recent actions by the U.S. Securities and Exchange Commission (SEC), we are edging closer to the future envisioned in the JOBS Act.

The SEC’s final rules implementing Title II of the JOBS Act, the Access to Capital for Job Creators Act, took effect on September 23, 2013. Those rules allowed investment in equity crowdfunding, but only for accredited investors, those with more than $200,000 income per year or a net worth exceeding $1 million, excluding the value of their primary residence.

Title III of the JOBS Act, the Crowdfunding Act, was supposed to allow any individual to participate in equity crowdfunding, but more than 2 years after the deadline mandated by Congress, Title III rules have not yet been finalized. The SEC released 585 pages of proposed rules back in October 2013, but there is considerable uncertainty about whether the Commission will meet its proposed agenda of issuing the final rules by October 2015. Moreover, because issuers using Title III crowdfunding will be limited to raising $1 million per year and won’t be able to engage in general solicitation, some critics have claimed that trying to implement this form of crowdfunding will be more time-consuming and expensive than it will be worth.

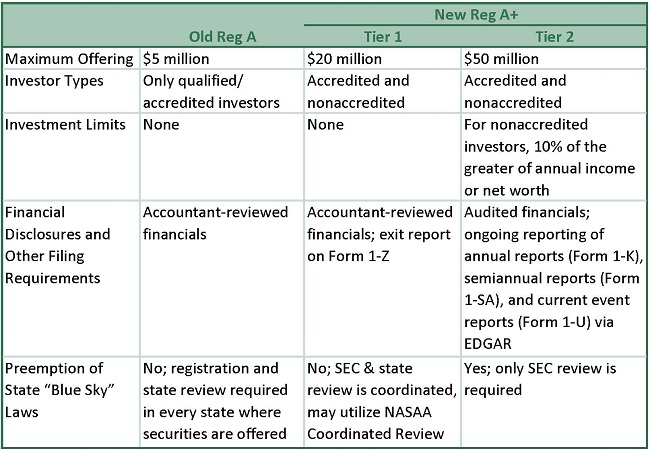

However, on March 25, the SEC approved final rules updating and expanding Regulation A, an existing exemption from registration under the Securities Act of 1933 for issuers of less than $5 million of securities in any 12-month period. The new rules, often referred to as Regulation A+ or Reg A+, were mandated by Title IV of the JOBS Act, the Small Company Capital Formation Act. The Reg A+ final rules were published in the Federal Register on April 20 and take effect on June 19.

The new rules expand Regulation A into two tiers. Tier 1 offerings will be more similar to the previous Regulation A offerings, but the maximum offering has been increased to $20 million in a 12-month period, including up to $6 million on behalf of security holders that are affiliates. Tier 2 raises the maximum offering to $50 million in a 12-month period, including up to $15 million on behalf of affiliates. All Reg A+ issuers must file balance sheets and other required financial statements for the two most recently completed fiscal years. Tier 1 financial statements do not need to be audited unless the company has already obtained an audit for another purpose, but Tier 2 offerings must provide audited financial statements. Reg A+ offerings will not be integrated with prior offers or certain subsequent offers of securities. So, for example, a company could conduct a Regulation D offering, then a Regulation A+ offering, and the two offerings would not be integrated.

Aside from the increased maximum offerings, one of the advantages of Regulation A+ is that it broadens the definition of “qualified investors” to include non-accredited investors, although there is a cap on how much they can invest in a Tier 2 offering. Non-accredited investors can invest a maximum 10% of their income/net worth per year, protecting these often less experienced investors and making it so that they cannot “lose it all” with a single crowdfunded investment. However, Reg A+ investors will be able

to self-certify their income or net worth, which simplifies the process.

Summary of Regulation A+

Another advantage is that Tier 2 offerings benefit from federal preemption of state “Blue Sky” laws, requiring only SEC review. Being able to skip state registration and review should reduce the administrative burden and expense considerably, and is expected to be a strong perceived benefit of Tier 2 Reg A+ offerings. Tier 1 will remain subject to both SEC and state review, although these offerings will be able to take advantage of the North American Securities Administrators Association (NASAA) Coordinated Review Program.

One more benefit of the Reg A+ offerings is that securities sold under Reg A+ would not be considered “restricted securities” under Securities Act Rule 144 and could therefore be traded freely. This could lead to development of a secondary market for these securities, which would solve the liquidity problems incurred by many crowdfunded investments. It’s generally much easier for companies to attract investors with liquid offerings, so that would be a big advantage. Another advantage is that liquidity offers investors a better sense of the market value of these investments, something that was missing in prior crowdfunded investments.

There’s one more area of crowdfunding in which we’ve seen some exciting developments. In a previous post, we mentioned that several states had already enacted or were considering enacting crowdfunding exemption laws to facilitate intrastate investment offerings, which are already exempt from SEC regulation. These intrastate crowdfunding investment regulations have become increasingly popular; 18 states plus the District of Columbia have now adopted their own crowdfunding statutes, and 21 other states are considering such legislation.

Keep an eye on the blog, and we will continue to post updates on the evolving crowdfunding regulations and other investment news.

{kind=link}

Recent Comments